Navigating Jumbo Loans: Key Considerations Before Taking A Loan

Considering purchasing your dream home? Understanding jumbo mortgage loans is essential, though approval is based on meeting specific criteria. This article breaks down jumbo loans in simple terms, helping you understand key aspects like loan limits, mortgage rates, and down payment requirements.

We'll explore potential financing solutions for high-value homes, providing you with comprehensive information to help you navigate the complex landscape of jumbo loans, supporting your decision-making process.

A jumbo loan is a type of mortgage that exceeds the conforming loan limits established by federal agencies such as Fannie Mae and Freddie Mac. These limits generally start at $726,200, though they can be higher in pricier areas. Designed for financing high-value homes, jumbo loans accommodate larger borrowing needs but are subject to stringent approval processes.

The main differences from conventional loans include stricter loan qualification criteria. Jumbo loans usually require higher credit scores, larger down payments (often 20% or more), and more extensive documentation to prove financial stability.

Additionally, interest rates on jumbo loans can be higher than those for conventional loans due to the increased financial risk to lenders. However, they offer the advantage of financing larger amounts, making them ideal for property investment in luxury markets. Understanding these distinctions is crucial for buyers considering high-value properties.

Jumbo loans can offer significant advantages for those purchasing high-value properties, featuring higher loan limits which allow for the financing of more expensive homes. However, these benefits are subject to borrower qualification and market conditions.

This flexibility might enable purchases in luxury real estate markets. Consult with Carlyle Financial to understand your options. Also, jumbo loans can be tailored to meet specific needs, offering options that standard loans might not provide.

Benefits of opting for a Jumbo Mortgage Loan:

Jumbo loans, while beneficial for financing high-value properties, come with some drawbacks. First, they have stricter qualification criteria, requiring higher credit scores, larger down payments, and extensive financial documentation.

This can make it harder for some borrowers to qualify. Second, jumbo loans often come with higher interest rates compared to conventional loans, leading to increased monthly payments and overall loan costs..

Things you might want to consider before opting for a Jumbo Mortgage Loan:

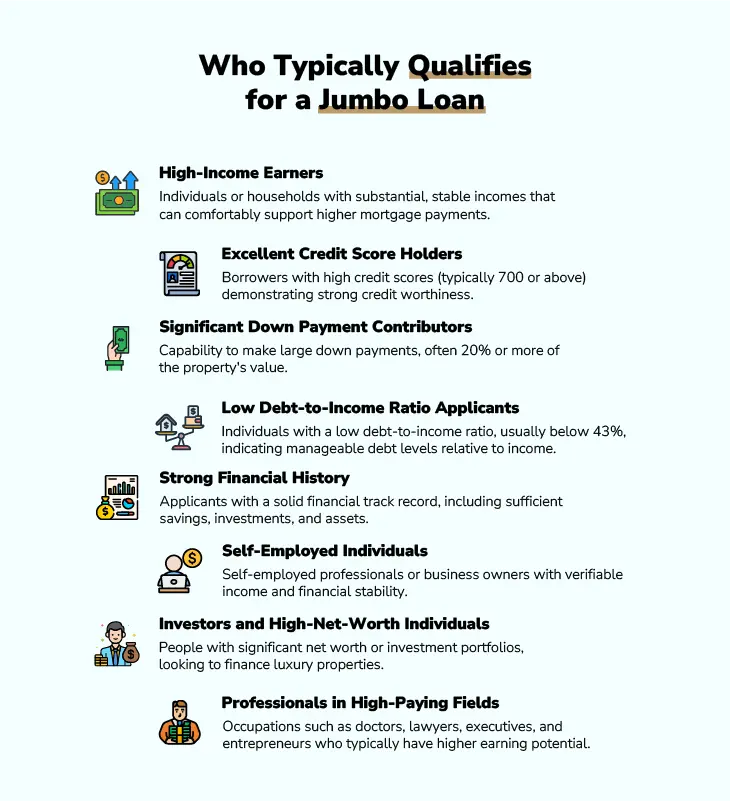

Qualifying for a jumbo mortgage loan involves a few important steps. First, you'll need a high credit score, usually 700 or above, to show lenders that you're a trustworthy borrower.

Next, you'll need to prove you have a steady, substantial income. This means providing tax returns, W-2s, and recent pay stubs. If you're self-employed, you might need extra documents.

Finally, jumbo loans typically require a larger down payment, often 20% or more of the property's value. This helps show you have a good amount of equity in the home from the start.

Understanding Interest Rates and Loan Terms for Jumbo Mortgages

Interest rates and loan terms are crucial to understand when considering a jumbo mortgage. Understanding these basics can help you choose the right loan for your luxury home purchase:

How Interest Rates are Determined: Interest rates for jumbo loans depend on various factors, including your credit score, down payment size, loan amount, and market conditions. Lenders assess these to determine your interest rate, which impacts your monthly payment and overall loan cost.

Fixed vs. Adjustable Rate Mortgages: There are two main types of interest rates: fixed and adjustable. Fixed-rate mortgages have the same interest rate for the entire loan term, providing consistent monthly payments. Adjustable-rate mortgages (ARMs) start with a lower fixed rate for a few years and then adjust periodically based on the market. ARMs can save money initially but might become more expensive if rates rise.

Understanding Loan Terms: Loan terms refer to the length of time you have to repay the loan, usually 15, 20, or 30 years. A longer term means lower monthly payments but more interest over the life of the loan. A shorter term has higher monthly payments but saves on total interest paid.

Final Thoughts on Jumbo Mortgage Loans

Understanding the complexities of jumbo loans, from the impact on your credit score to the terms of repayment, is essential. It's important to consult with qualified mortgage professionals to navigate the loan approval process effectively, tailored to your specific financial needs.

Contact Carlyle Financial to discuss options that fit your needs.

Jumbo mortgages can be complex, especially for first-time borrowers or those unfamiliar with high-value home loans. Jumbo mortgages, also known as non-conforming loans, are designed for properties that exceed the conforming loan limits set by the Federal Housing Finance Agency (FHFA).

Buying your first home is both exciting and a little overwhelming, especially when you’re unsure how long the mortgage process will take. Each step, from pre-approval to closing, can vary in timing, but having a clear understanding of each stage will help you prepare and make the process more manageable.

An interest-only mortgage is exactly what it sounds like: a type of loan where, for a set initial period of time (the first few years of your loan), you’re only paying the interest, not the principal loan.

Secure financing through our exclusive network of local community banks and specialty lenders.